As 2026 begins, Chinese foreign trade practitioners stand at the crossroads of a profound transformation. The cancellation of export tax rebates, Mexico’s tariff hikes, and the full implementation of the EU’s Carbon Border Adjustment Mechanism—three seemingly independent pieces of news—collectively point to an unavoidable reality: the era of rough expansion driven by low prices and high volume has come to an end.

I. Cancellation of Export Tax Rebates: A Top-Down Reckoning Against “Involution”

On January 8, the Ministry of Finance and the State Taxation Administration jointly issued an announcement canceling export tax rebates for photovoltaic products and other goods, and will gradually reduce until eventually canceling export tax rebates for battery products. This adjustment covers a wide range of sectors, including not only photovoltaics but also chemical raw materials and products (basic chemical raw materials, organophosphorus compounds, etc.), plastic PVC and polymers, kitchen utensils, ceramic products, silicones, cement, glass products, and other industries.

The original intent of export tax rebates was to avoid double taxation. However, when Chinese companies find themselves trapped in a vicious cycle of “no orders without price cuts, no profits with price cuts,” when overseas markets wield tariff sticks under the pretext of “dumping,” and when state financial subsidies end up fueling low-price competition—canceling rebates becomes not only a necessary move to break the deadlock but an inevitable policy choice.

What deserves deeper consideration from foreign trade professionals is the “anti-involution” signal released behind this move. Chinese enterprises have never experienced the Western stage of “pouring milk into rivers” to eliminate overcapacity; they are accustomed to expanding production tirelessly and competing on volume. But global demand growth has long failed to keep pace with capacity expansion. Traditional industries like steel, cement, and light manufacturing have been mired in difficulties for years, and now emerging sectors such as photovoltaics, lithium batteries, new energy vehicles, and e-commerce platforms are also struggling to escape the death spiral of homogeneous competition.

The state’s move this time aims to forcibly interrupt this vicious cycle. It is foreseeable that this is by no means an isolated case, nor will it be the final one. Considering previous actions such as the “complete termination of buyer-paid export” and “tax compliance for cross-border e-commerce,” the future picture has become clear: a batch of non-compliant small and medium-sized enterprises will be cleared from the market, a wave of excess capacity will be forcibly eliminated, and numerous involutionary industries will undergo structural adjustments featuring production reduction, capacity limitation, and price increases.

Behind this reckoning lies the difficult transformation of Chinese manufacturing from “cost-driven” to “value-driven.” The surviving enterprises must learn to earn premiums through technology, branding, and supply chain efficiency.

II. Mexico’s Tariff Hikes: The “Exclusionary” Reconstruction of the North American Supply Chain

On December 29, 2025, the Mexican government published a detailed list in the Federal Gazette of tariff increases on imported goods from countries without free trade agreements. Effective January 1, 2026, tariffs on 1,463 products have been raised, with Chinese goods bearing the brunt.

The essence of Mexico’s move is a “letter of allegiance” submitted to the United States. By aligning its trade policies with Washington, Mexico hopes to secure a more advantageous position in the restructuring of the North American supply chain while avoiding the risk of trade friction with the US.

However, there are more dangerous undercurrents beneath the surface. Lin Xueping, a visiting researcher at Shanghai Jiao Tong University, pointed out sharply: “The United States is using its powerful domestic consumer market (import quotas) as a strategic tool to reshape the global manufacturing landscape.” The tariff war showdown between China and the US is just the obvious line; the hidden line is the US using tariffs as leverage to coerce allies, isolate China, and reconstruct the supply chain map.

Trump’s style of governance adds more uncertainty to this situation. As recently as January 17, he threatened to impose tariffs on eight European countries until the US successfully “acquires” Greenland—in his hands, tariffs serve as both an economic weapon and geopolitical leverage.

This systemic turmoil not only directly impacts China-US and China-Mexico trade but also poisons the normal economic and trade environment between China and other countries. To avoid geopolitical risks, multinational purchasers prioritize supply chain risk management over cost considerations. The “1+N” strategy has become standard: China is just one of the supplier options, with backup production capacity simultaneously deployed in Southeast Asia, South America, and other regions.

Facing this changed landscape, foreign trade practitioners must adjust their expectations: shrinking global demand, geopolitical interference in trade, and high export barriers will become the new normal. The way forward lies in a two-pronged approach—enhancing the irreplaceability of products on one hand, and on the other, dispersing tariff risks through overseas factory construction and expanding into diversified markets to hedge against dependence on any single market.

III. EU CBAM: Trade Barriers Under the Guise of “Green”

On January 1, 2026, the EU’s Carbon Border Adjustment Mechanism (CBAM) ended its transitional period and officially took effect. Imports of high energy-consuming products such as steel, aluminum, cement, fertilizers, electricity, and hydrogen must declare carbon emission data or purchase CBAM certificates, paying corresponding fees based on carbon emissions.

Nominally, the carbon tax is paid directly by European importers. However, the chain of cost pass-through will inevitably extend to Chinese suppliers. Enterprises need not panic excessively, but they must prepare in advance.

Looking deeper, CBAM indicates an irreversible trend: carbon emissions are transforming from an environmental issue into a trade weapon. Besides the EU, countries like the US and Japan are also brewing similar mechanisms, and a global “carbon rules” system is taking shape.

Foreign trade professionals need to see the “two layers of truth” in CBAM:

The first layer is the “green barrier.”

The core principle of UN climate governance is “common but differentiated responsibilities”—developed countries, due to their historical emissions and higher development levels, should bear more emission reduction obligations. The EU’s unilateral imposition of a “one-size-fits-all” carbon standard essentially locks developing countries that have not yet mastered low-carbon core technologies into the middle and low end of the global value chain, constituting unfair competition for major manufacturing countries like China and India.

The second layer is the “green alliance.”

CBAM grants exemptions to EU member states and European Economic Area countries like Iceland and Norway, while promoting “rules mutual recognition” with allies such as the US and Japan, offering their products exported to Europe flexible arrangements and cost reductions. The essence of this mechanism is to build a trade alliance with carbon rules as the bond, achieving the dual goals of trade protection and camp division.

Faced with this change, at the national level, China needs to compete for discourse power in carbon rule-making; at the enterprise level, foreign trade professionals must early on layout carbon asset management and promote green and low-carbon transformation to gain an advantageous position in future global trade.

IV. The Path to Breakthrough: Navigating Changes with Technological Innovation

The three major policy signals collectively point to a fundamental shift: the underlying logic of foreign trade has been rewritten.

2026 is destined to be fraught with pain. The latest WTO outlook has significantly lowered its global merchandise trade growth forecast for this year to 0.5%. But amidst the pain lies opportunity—this year may very well be the “window of opportunity” for proactive positioning and seizing the initiative in the coming years.

The new rules impose new requirements on foreign trade enterprises: enhancing product added value, building diversified markets, deeply cultivating localized operations, and accelerating green transformation. In this difficult breakthrough from “price war” to “value war,” a group of Chinese enterprises are taking the lead by leveraging technological innovation.

Multifit Solar stands as a typical example among them. As a high-tech manufacturing enterprise specializing in the R&D, production, sales, and construction of solar power generation systems and other green energy technologies, Multifit was established in 2009, headquartered in Beijing, with its production base located in the Shantou High-tech Industrial Development Zone, Guangdong Province.

After more than a decade of deep cultivation, Multifit has built a comprehensive quality management and technology R&D system. It has obtained ISO9001 Quality Management System Certification, ISO14000 Environmental Management System Certification, OHSMS28001 Occupational Health and Safety Management System Certification, CE Certification, FCC Certification, and holds over 80 items of independent intellectual property rights, patents, and software copyrights.

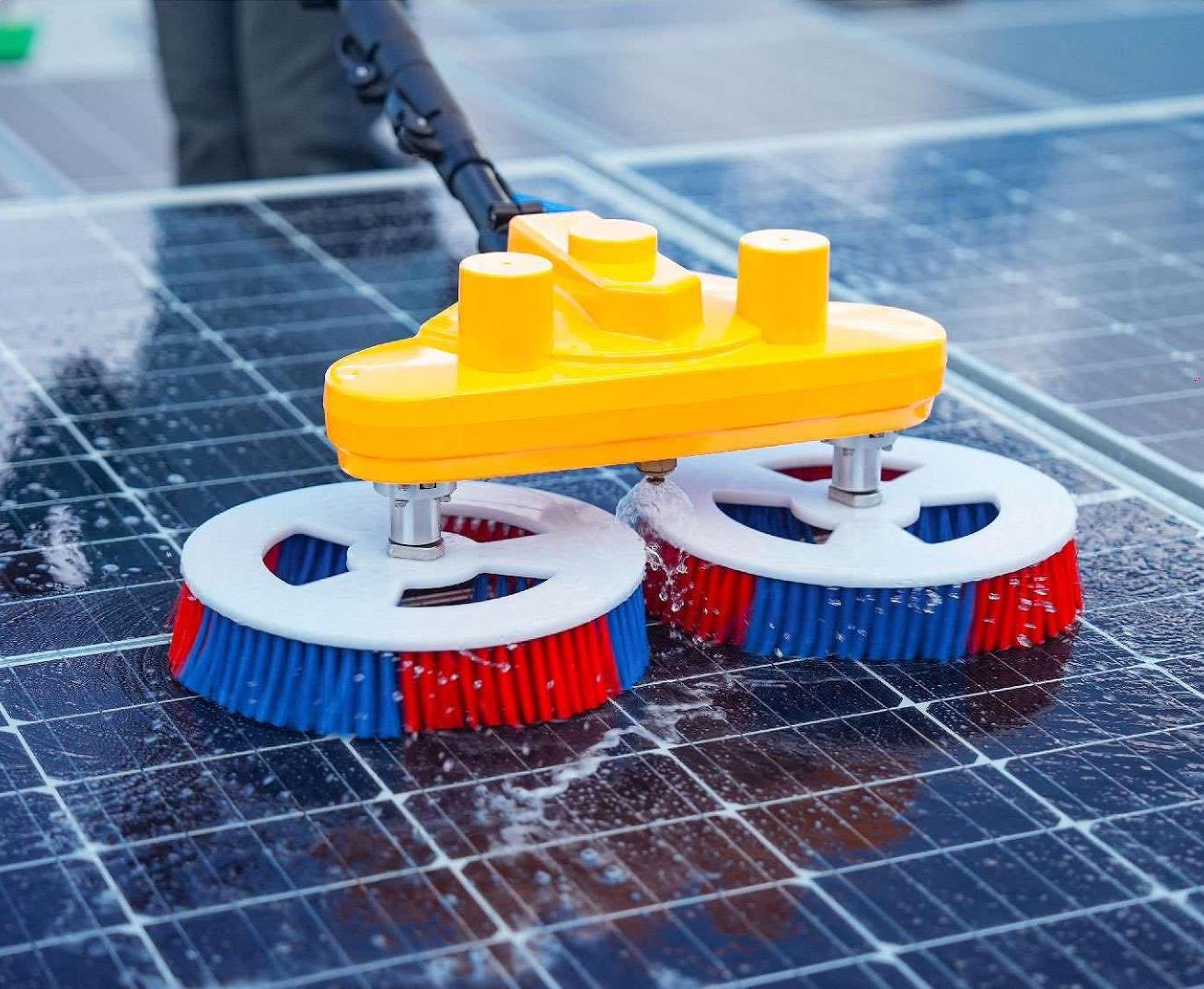

Amidst the homogeneous competition deeply entrenched in the photovoltaic industry, Multifit has chosen a path of differentiated breakthrough. The company’s independently designed and developed solar panel cleaning robots can increase the power generation efficiency of solar panels by 8% to 30%, while effectively avoiding equipment damage caused by hot spot effects, creating incremental value for customers from the two dimensions of “efficiency enhancement” and “protection.” Currently, Multifit cleaning robots serve numerous power stations, with a cumulative served installed capacity exceeding 500 megawatts.

Targeting different application scenarios, Multifit has created a rich matrix of cleaning equipment:

Tracking Solar Panel Cleaning Robot: Adapts to commercial & residential power station cleaning.

Automatic Right & Left Solar panel Cleaning Robot: An automated cleaning solution suitable for large-scale ground & rooftop power stations.

Semi-Automatic Solar Cleaning Brush: A lightweight solution targeting residential distributed power stations.

It is precisely this shift in mindset from “selling products” to “selling solutions” that allows Multifit to carve out a development path relying on technology premiums rather than cost advantages in the deeply involuted photovoltaic track.

Facing the “anti-involution” pressure from canceled rebates, the “siege” crisis of Mexican tariffs, and the “green barriers” of the EU CBAM, Multifit Solar uses core technology as its spear and green low-carbon practices as its shield, responding to the industry dilemma of “low-price competition” with the unique value of “improving power generation efficiency.” This echoes the core judgment of this article: in an era where old rules are collapsing, only value creation can ensure survival.

This is precisely the stance Chinese manufacturing should adopt to navigate changes and break through new rules.

Post time: Mar-05-2026